The UEMOA banking sector faces mounting risks as outlined in the January 2026 economic outlook report, with Niger emerging as a stark outlier. While the regional financial system navigates symbolic milestones, the country’s alarming non-performing loan (NPL) rate underscores a deepening rift within the monetary union.

Niger: A Distress Signal in Regional Banking Stability

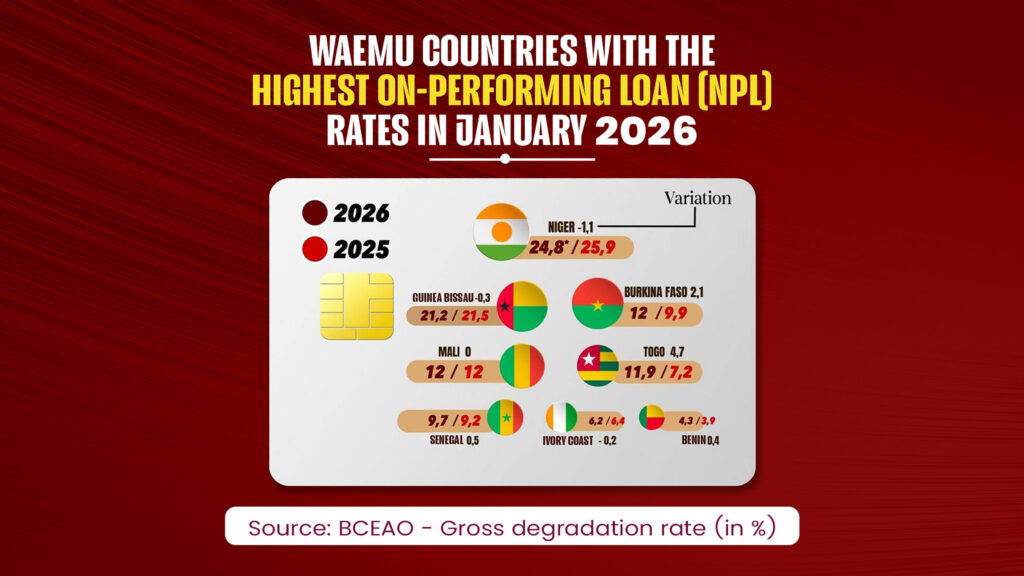

Despite marginal improvements, Niger remains the weakest link in the UEMOA banking chain. The nation’s NPL rate stands at a staggering 24.8% in January 2026, the highest in the region, indicating that nearly one in four loans granted in the country is in default.

While this figure shows a slight decline from 25.9% in 2025, the gap between Niger and the regional average highlights an unprecedented exposure to risk. This vulnerability is exacerbated by persistent security threats and political instability, which continue to undermine investor confidence.

UEMOA’s Two-Speed Economic Divide

January 2026 data reveals a sharp divide between coastal economies and the Sahel bloc, where Niger sits at the epicenter of the crisis.

The Sahel: A Region Under Financial Pressure

Niger is not alone in facing severe financial distress. The broader Sahel region grapples with elevated NPL rates:

- Mali and Burkina Faso: Both nations report a 12% NPL rate, with Burkina Faso experiencing a concerning annual increase of 2.1 percentage points.

- Guinea-Bissau: The country remains in critical territory with a 21.2% non-performing loan rate.

The Coastal Bloc: Relative Resilience Amidst Challenges

In contrast, coastal economies demonstrate greater financial stability, though some cautionary signals persist:

- Benin: Leads the union with the lowest NPL rate at 4.3%.

- Côte d’Ivoire and Senegal: Maintain stability with rates of 6.2% and 9.7%, respectively.

- Togo: Stands out with a sharp rise in bad loans, jumping from 7.2% to 11.9%—a 4.7-percentage-point increase.

A Credit Boom Overshadowed by Rising Defaults

Total outstanding loans in the UEMOA region have surpassed 40.031 trillion CFA francs, marking a 4.7% year-on-year increase. However, this growth is clouded by a troubling rise in non-performing loans, which now total 3.631 trillion CFA francs.

The coverage ratio has dropped to 59%, signaling that banks are struggling to keep pace with the surge in defaults, leaving their financial buffers stretched thin.

Banks Tighten the Screws as Risk Perception Worsens

The deteriorating credit landscape has prompted banks to adopt stricter lending policies:

- Stricter lending criteria: Higher personal contributions and more rigorous collateral requirements are now standard.

- Selective credit expansion: Banks are prioritizing balance sheet security over lending growth, which risks stifling financing for local SMEs and SMEIs.

As the UEMOA banking system stands at a crossroads in early 2026, the precarious situation in Niger and the spread of financial risk across the Sahel demand heightened vigilance. Failure to address these challenges could trigger a liquidity crisis with far-reaching regional consequences.