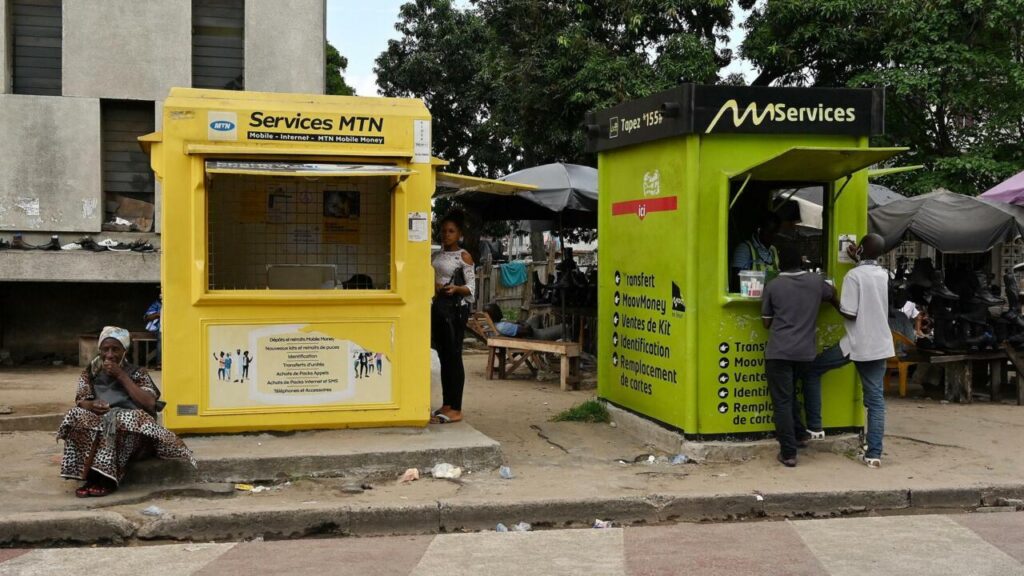

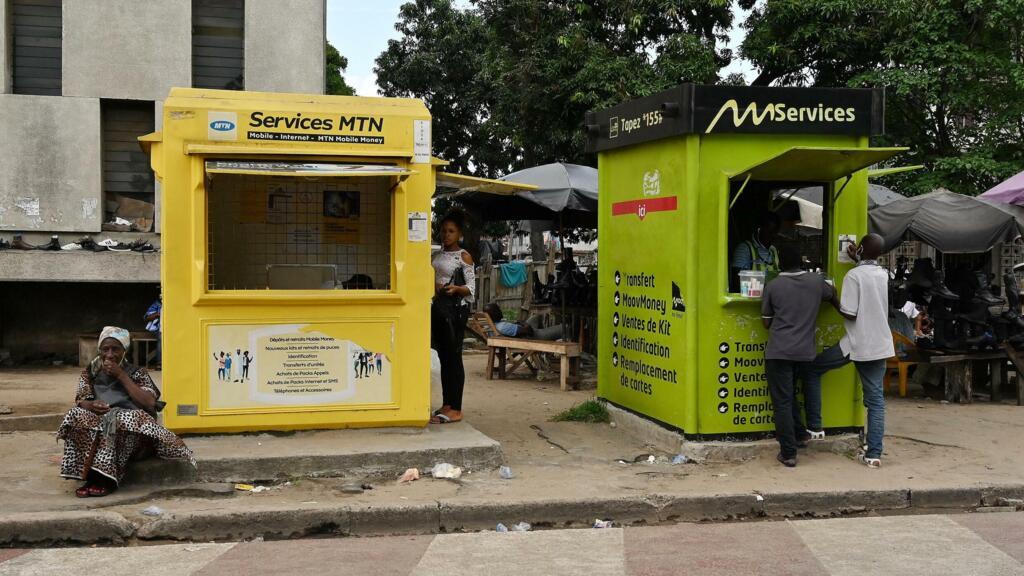

Mobile money transfer agencies are seen on May 6, 2020 in a district of Abidjan in the Ivory Coast. (Photo by ISSOUF SANOGO / AFP)

A Vital Service Under Strain

In Côte d’Ivoire, mobile money kiosks have become an indispensable part of the financial landscape. With over 400,000 service points now active, according to the Agency for the Promotion of Financial Inclusion, they outnumber traditional ATMs by a staggering 300 to one. Ivorians rely on these booths for everything from depositing their salaries to withdrawing funds for daily needs. However, the agents who run these essential services are increasingly grappling with a critical problem: a shortage of physical cash that hampers their operations.

Late afternoon in the bustling Angré Château neighborhood of Abidjan illustrates the issue perfectly. It’s a peak time for errands and commuting, but at a busy intersection, a mobile money booth has run out of banknotes. A customer named Rosette, hoping to withdraw 10,000 CFA francs (about 15 euros), is resigned to the situation. “When you arrive, they don’t have what you need. It happens, so we just have to deal with it,” she says.

Inside the yellow kiosk, the teller, Nema, tries to manage customer expectations. “Some days see a lot of withdrawals, and we can run out of cash. We apologize and inform clients that we can only accept deposits for now.”

Lost Customers and Diminished Profits

Rather than wait, many customers simply move on to find another agent. For Affoué, the manager of the booth and a former accountant, every lost transaction is a direct hit to her bottom line. “You lose the customer, and you lose the commission from that customer,” she explains. “That’s why it’s crucial to serve clients well, so commissions can grow and we can turn a clear profit.”

The commissions paid by major operators like Orange, Moov, MTN, and Wave are modest. For a 10,000 CFA franc (15 euros) transaction, an agent might earn between 20 and 60 CFA francs (3 to 9 euro cents). Profitability, therefore, depends on a high volume of transactions, both large and small. When cash or electronic credit runs dry, the entire business model falters. Agents are forced to temporarily shut down to replenish their stock at a bank or operator branch, losing valuable business hours.

Motorbikes as a Lifeline

To tackle this liquidity gap, an Abidjan-based startup named Leya has developed a rapid-response service. Gertrude Yapi, Leya’s director of operations, outlines their model, which uses motorcycle couriers to assist mobile money service points. “We supply them with electronic credit in under four minutes and deliver cash in less than 30 minutes to satisfy their clientele,” she states. “This allows sales points to increase their turnover by an additional 50%.” The service has gained traction, with Leya now serving over 3,000 active clients across four major Ivorian cities: Abidjan, Bondoukou, Bouaké, and Korhogo.

According to Ivorian economist Kassoum Timité, ensuring service continuity is vital for the broader economy. “Mobile money directly serves the population in the informal sector, which makes up the largest part of economic activity in Côte d’Ivoire,” he notes. This sector is estimated to account for as much as 40% of the gross domestic product. “Therefore, a lack of liquidity will slow down transactions, and economic activity will also decline.”

The stakes are high. In 2024, daily mobile money exchanges surpassed 140 billion CFA francs (over 210 million euros), a nearly fourfold increase from 2020, highlighting the sector’s explosive growth and the critical need to resolve its operational challenges.